As we all know, in today’s data-rich world we are constantly inundated with information in bite-sized chunks – whether it is on the internet, social media or on our favorite television news channel. People just don’t have the attention spans they used to when it comes to consuming information.

Sit at an underwriting desk in any insurance company and you will notice the same trend – people are extremely busy and they simply don’t have the time to process massive amounts of information about a risk when making important underwriting and pricing decisions. Some of this is a by-product of our social environment, but this is also driven by company objectives to ‘do more with less’ and operate at optimal levels of efficiency.

In order to address this, many loss control teams are shifting their loss control reporting approach to report on risks ‘by exception’ which means the field team is focusing on (1) what makes this risk different from other comparable risks in a similar class and (2) what needs to be done in order to improve the quality of this risk (i.e. requirements/recommendations or a risk improvement plan). The reality is, when an underwriter is short on time and they are presented with a lengthy loss control report, they will flip directly to the overall commentary on the risk and the section which outlines proposed actions for risk improvement.

To help support the initial triage process (i.e. determining which reports go to the ‘top of the pile’), it is helpful to include a visual depiction of the overall quality of the risk to provide a high level snapshot to the underwriter as to whether or not this report requires extra attention. This can be effectively shown (even in the absence of an advanced loss control system) using a colored rating system (e.g. green/yellow/red) or a numerical breakdown (e.g. 72/100) and to take it one step further, may also be broken out into sub-categories to further identify specific areas of potential risk improvement. For property risks, these may include construction, fire protection and specific hazards. In the workers compensation arena, key sub-categories would include safety commitment/culture, safety programs, personnel practices and controls.

Along a similar vein, we always encourage our clients to think of analyzing risks first generically and then build on top of this generic analysis with whatever additional modules or supplements may be required depending on the specific type of risk. In practice, whether a loss control consultant is servicing a transportation company, a food processing plant or a commercial farming operation, the initial analysis is the same. There are great advantages to this from a productivity perspective, but even more powerful are the data mining and analysis benefits.

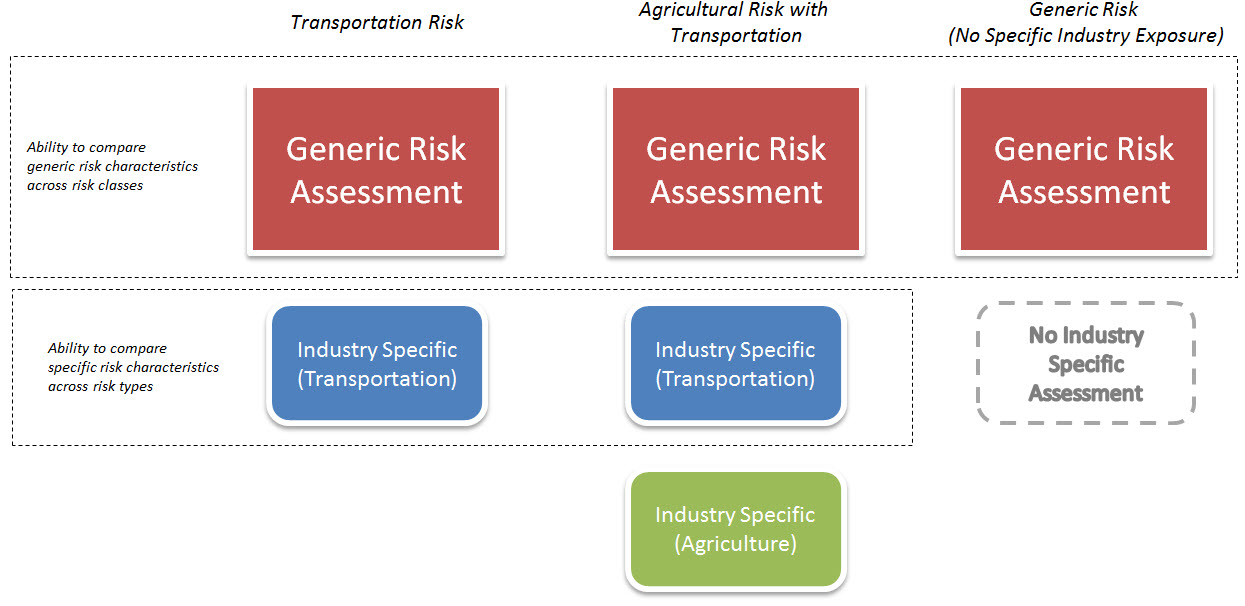

The below graphic illustrates an example of this approach where the complete risk analysis for any given risk is compiled of various components as required.

By utilizing this approach, data can be analyzed across different types of risks based on the specific details contained within the generic loss control assessment. This assessment will include information such as the operational and managerial aspects of the risk which can be used consistently across all (or most) types of risks. The loss control consultant will then select additional components or supplements depending on the specific characteristics of the risk. In the above example, although one risk is a pure transportation operation and the other is an agricultural risk with some transportation exposure, this component-based approach will facilitate more robust comparative analysis down the road.

In terms of the content of these assessment forms and various granular components, it is worth reiterating the overall theme of this article; less is more. The industry is shifting away from collection of large amounts of (often redundant) detailed data and the current best-practice in this area asks loss control consultants to consider whether the exposure being analyzed is in line with other standard risks in this category. If not, what specifically makes this risk more desirable or less desirable (and if less, what needs to be done in order to bring the risk closer to par).

In a future segment, we will explore in more detail the nuts and bolts behind the risk assessment and loss control recommendation management process within a loss control management system. Traditionally, this has been left to the opinion and expertise of the loss control consultant, but a trend has been emerging over the last few years which reduces this subjectivity and enforces a more quantitative approach to the risk analysis.